Import Patterns Suggest Renewed Supply Movement Entering 2026

Executive Interpretation

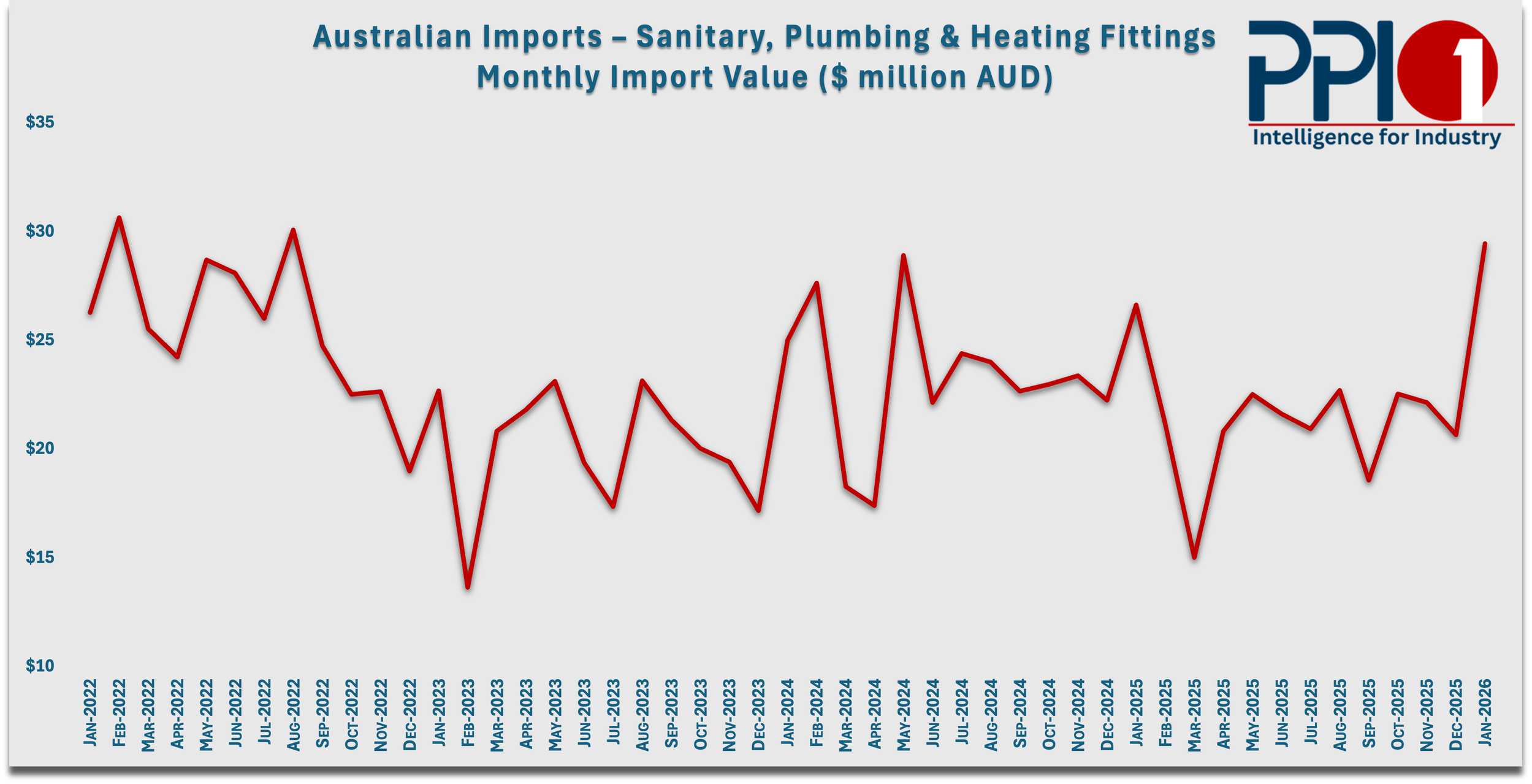

Import values across sanitary, plumbing and heating fittings remained volatile across the reporting period, with several pronounced peaks above $28 million and periodic declines into the mid teens, indicating ongoing fluctuations in shipment timing, landed stock arrivals and importer purchasing cycles. The sharp lift recorded at the latest point suggests renewed stock movement entering the market after a softer preceding period, likely reflecting delayed shipments, year opening replenishment activity, or importer positioning ahead of upcoming sales cycles.

For sanitaryware and plumbing product businesses, this pattern is commercially important because elevated import months often signal intensified market supply, stronger competitor stock positions, and potential pricing pressure in downstream channels. Businesses should monitor whether this latest uplift continues over coming months, as sustained higher import levels may indicate stronger forward inventory confidence across wholesalers, merchants and project supply channels.

Disclaimer: Source data is drawn from official Australian trade datasets and interpreted by PPI Group for market intelligence purposes. Product classifications may capture broader product groupings beyond individual sanitaryware and plumbing lines. Reported values should be treated as directional indicators rather than exact market share or demand measures.

-

Import values across sanitary, plumbing and heating fittings continue to show pronounced monthly movement, with several high value periods indicating that imported stock remains active across the Australian market. While month to month changes should not be read as direct demand shifts, repeated elevated import periods suggest that significant product volumes are continuing to enter local supply channels. For sanitaryware businesses, this can influence pricing conditions, distributor stock levels and competitive positioning where imported product overlaps directly with core product categories.

Note: Review disclaimer first.

-

Where elevated import values persist across multiple reporting periods, businesses should consider whether competing product may already be moving into merchant, project or wholesale channels ahead of confirmed sales demand. This can affect margin flexibility, timing of local stock releases, and the level of discount pressure likely to emerge across price sensitive categories during active trading periods.

Note: Review disclaimer first.

-

PPI One draws on a range of recognised Australian and international reference sources to support industry reporting, market interpretation and technical intelligence. This includes official government trade datasets, market intelligence publications and regulatory source material used to strengthen context across product, commercial and technical reporting.

Core reference sources currently include the Australian Bureau of Statistics for trade and economic indicators, the Department of Foreign Affairs and Trade for merchandise trade data, IBISWorld for broader industry market context, and public regulatory data including WELS and the Australian Building Codes Board where relevant.

PPI Group interprets and structures these sources specifically for the plumbing products sector, allowing members to view broader market signals through an industry relevant lens rather than relying on raw datasets alone.

Note: Review Disclaimer First.

-

This report uses publicly available Australian merchandise trade data aligned to the selected product classification covering sanitary, plumbing and heating fittings. The category includes a broader product grouping than sanitaryware alone and should therefore be interpreted as a broad import activity indicator rather than a precise sanitaryware only market measure. Monthly values may also reflect shipment timing, customs processing and importer consolidation patterns.

-

The next reporting cycle should be watched closely to determine whether recent higher import values continue or return to lower operating ranges. A second consecutive elevated month would suggest sustained inventory positioning, while a sharp correction may indicate isolated shipment timing rather than broader commercial movement. Particular attention should also be given to whether similar movements appear across related product categories.

Note: Review disclaimer first.